Long Put Options Strategy: Beginner’s Guide

The long put is a defined risk, low-probability, and bearish options strategy with limited profit potential.

Long put options are bearish market bets that profit when the underlying stock or index price falls below the strike price minus the premium paid. Although put options originally came into existence to hedge a portfolio or position against downside losses, today, they are mainly used by individual traders as vehicles for bearish speculation.

Put options give owners the right to sell 100 shares of the underlying stock at the strike price, offering downside exposure similar to shorting stock but with much lower capital requirements. This leverage can amplify potential returns, but time decay erodes the option's value as expiration approaches.

Highlights

- Long put option: Low probability, defined-risk bearish options trade

- Underlying Asset: The security you are purchasing the put on

- Strike Price: The price at which you can sell the stock

- Expiration Date: The date on which your option contract expires.

- Premium: How much a put option costs.

Long Put: Car Insurance Analogy

If you understand car insurance, you already understand how put options work.

Suppose you bought a brand-new Cybertruck for $100,000 and took out an insurance policy with a $2,000 annual premium.

A month later, you’re walking down Michigan Avenue when a Cybertruck—just like yours—speeds off. You glance back. Your parking spot is empty.

You call your insurance company, and they write you a check to cover the cost of the stolen Cybertruck (if only it were that easy!)

In this scenario, you bought car insurance, which acts like a ‘put’ option, to protect yourself against financial loss.

That’s what put options are - insurance policies you can take out against a stock, ETF, or index.

Long Naked Put Options

Many individual traders do not buy put options to protect a position (referred to as a 'protective put') - they buy put options for bearish speculation. Going ‘long naked’ means your long put is not hedged with other options (vertical spread) or stock.

You don’t need to own stock or an ETF to buy a put option against it. It’s like a side bet or taking out an insurance policy on a car you don’t own. If that car crashes, you’ll get paid out. If it doesn’t, your option will not be profitable. Options are called derivatives because their value is not inherent but derived from the underlying asset.

Long Put Option: Max Profit

The maximum profit on a naked long put option equals the put's strike price minus the price (premium) paid.

For example, let’s say we have bought a 60 strike price put option on XYZ for $5, the strike price being the price at which we can sell the underlying XYZ stock.

Here are our trade details:

- Put Option Strike Price: $60

- Premium Paid: $5

- Max Profit: $55 (Strike Price - Premium Paid)

If XYZ drops to $0, the put is worth $60, but after subtracting the $5 option premium paid, the net profit is $55. What are the odds of achieving a max profit on a long put? Almost zero, as stocks rarely crash to $0.

Long Put Option: Max Loss

The maximum loss on a naked long put option is limited to the premium paid. This happens if the stock stays above the strike price at option expiration.

Let’s continue with the XYZ trade example:

- Put Option Strike Price: $60

- Premium Paid: $5

- Max Loss: $5 (Premium Paid)

If XYZ stays at $60 or higher, the put expires worthless, and the entire $5 premium is lost.

Long Put Option: Breakeven

The breakeven price on a long put option is the strike price minus the premium paid.

- Put Option Strike Price: $60

- Premium Paid: $5

- Breakeven Price: $55 (Strike Price - Premium Paid)

If XYZ closes at $55 at expiration, the put is worth $5, which exactly covers the cost of the option—no profit, no loss.

📖 Short Puts: Beginner's Guide

Option Basics

Before we get into a real-world trade example of a put option, it’s essential to understand four key components of options trading:

- Intrinsic/extrinsic value

- Time decay

- Moneyness

- Exercise/assignment

Let’s go! 🏃

Intrinsic vs Extrinsic Value

Two parts comprise an options price: intrinsic and extrinsic value.

- Intrinsic value: the amount of value an option has based on the stock's current price (how much the option is in the money).

- Extrinsic value: the amount of value an option has beyond intrinsic value, including time and volatility.

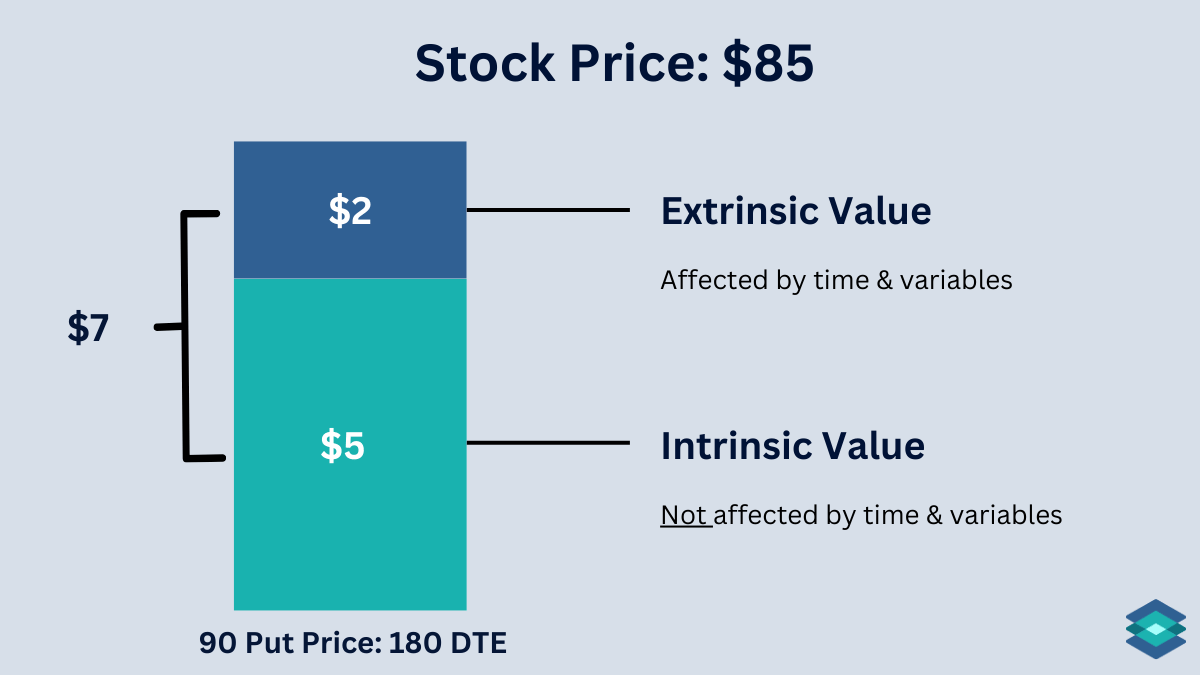

For example, let’s say we are long a 90 strike price put option on ABC that expires in six months. Here are our trade details

- Stock price: $85

- Strike Price: 90

- Option Price: 7

Since we own the 90 put option, we might expect its price to be $5—its intrinsic value, since it's in the money by that amount. However, as shown below, the option is actually priced at $7.

That extra $2 is the option’s extrinsic value, which comes from factors like volatility and time. With six months until expiration, a lot can happen!

By expiration, all extrinsic value disappears, leaving the option with only intrinsic value—if it’s in the money. If it’s out of the money, it expires worthless.

Put Options and Time Decay

Long option contracts steadily lose value in a flat market, assuming the stock price and implied volatility stay the same. Rookie traders are often caught off guard when their put option drops in value—even on days the stock is down. The problem here is the stock isn’t moving down fast enough to outpace time decay.

With each passing day, the chances of the stock falling to our strike price shrink. This time decay—known as theta in options trading—accelerates as expiration gets closer. You can see the effect below.

.png)

This is why most out of the money options will expire worthless. It’s very, very difficult to time the market. I know because I have tried myself many times!

Long Put: Option Moneyness

If you’re new to options trading, it may help first to read our guide on options moneyness here.

The strike prices of all put options fall into three categories:

- In-the-money (ITM): Strike price > stock price

- At-the-money (ATM): Strike price = stock price

- Out-of-the-money (OTM): Strike price < stock price

.png)

- The further out of the money a put option is (the lower the strike price relative to the stock price), the lower its chance of becoming profitable, so it’s cheaper.

- The further in the money a put option is (the higher the strike price relative to the stock price), the more likely it is to be profitable, making it more expensive.

We can see below on the TradingBlock platform how the price of put options diminishes as they retreat further out of the money.👇

Most retail traders prefer out of the money options because they are cheaper and offer the greatest return potential on investment. However, the further out of the money you go, the less chance your trade has of becoming profitable.

Another vital prerequisite of options trading is to understand how exercise and assignment works. 👇

Option Exercise and Assignment

- Exercise: The owner of a put option has the right to sell the underlying stock at the strike price.

- Assignment: When the option is exercised, the seller of the put option (also called the option writer) is "assigned," meaning they must buy 100 shares of stock per contract at the strike price.

At any point in time (for American-style options), owners of long put options can exercise their right to sell 100 shares at the strike price. For every long put, a short must purchase those shares when assigned.

📖 Exercise and Assignment: The Complete Guide

When Are Options Exercised/assigned?

Generally, only in the money put options are exercised since they let the holder sell stock at a higher price than the market. Exercising an out of the money put makes no sense—you’d be selling below market and taking an immediate loss.

The deeper a put is in the money, the more it makes sense to exercise. Its intrinsic value (strike price minus market price) is high, while extrinsic value (time and volatility) fades. Exercising a deep ITM put maximizes the long’s benefit since most of its value is intrinsic. With little extrinsic value left, holding it longer won’t add much.

Why not earn some interest or put another trade on with that cash?🤔

School is now out—let’s put on a trade!

Long SPY Put Trade Example

In our example, we will buy an out-of-the-money put option on SPY (SPDR S&P 500 ETF Trust) expiring in 3 months. Our intent is speculation and not hedging, so we do not own any existing SPY stock. We’re feeling lucky!

We chose this ETF because SPY offers:

- Broad market exposure

- High liquidity (tight spreads & high volume and open interest)

- Numerous strike prices and expirations

SPY Options Chain

Let’s go to the TradingBlock platform to find an option that works for us on the SPY options chain:

We decided to buy the 515 put option expiring on Dec 20 (88 days away) for 4.24. With the stock at $569, it’s a long shot.

Let’s get our order queued up and then send it:

SPY Trade Details

Here are our trade details:

Our SPY Position

- Position: Long 1 SPY Put Option

- Premium Paid: $4.24 ($424 total)

- Expiration: 88 days

- Strike Price: $515

- Current Stock Price: $569

- Breakeven Price: $510.76

This trade is a long shot.

We paid 4.24 for this put option, so for it to be profitable, SPY must drop from its current price of $569 to below our strike price of 515, minus the 4.24 premium we paid in 88 days. That means we won’t be profitable until SPY falls below 510.76. Here’s the math behind that:

- Breakeven Price = Strike Price−Premium Paid

- Breakeven Price = 515−4.24 = 510.76

We need the stock to drop by about 10% to break even! Have buyer's remorse yet?

SPY Long Put: Positive Outcome

Let’s fast forward 88 days to expiration. The economy is in shambles. The S&P 500 has plummeted 12%. The price of SPY has fallen from $569 to $500.

How did our long put do? Let’s find out!

- Expiration: 88 days → 0

- Strike Price: $515

- Stock Price: $569 → $500 📉

- Option Price: $4.24 → $15 📈

- Breakeven Price: $510.76 (unchanged)

The option we bought for $4.24 is now worth $15! Why? Because at expiration, the option is in the money by $15, which is purely intrinsic value.

Since it's expiration day, there's no time left, meaning no extrinsic value is left in the option. Remember that $15 actually represents $1,500 in value because each option contract represents 100 shares.

Subtracting the initial investment of $424 (the premium paid) from the $1,500, we can determine our net profit to be $1,076.

SPY Long Put: Negative Outcome

88 days have passed, and SPY has done nothing, which is a far more likely outcome. Here’s where we’re at on expiration:

- Position: Long 1 SPY Put Option

- Strike Price: 515

- Option Price: $4.24 → $0 📉

- Expiration: 88 days → 0

- Stock Price: $569 → $570 📈

The 525 put option we bought for $4.24 is now worth $0. Why? Because at expiration, the option is out of the money. With the stock at $570 on expiration, why would anyone want to sell SPY at our strike price of $515?

Our option has neither intrinsic nor extrinsic value. The option is worthless.

How To Exit A Long Put

There are four ways to exit a long put position:

- Trade out anytime before expiration in the open market

- Let the option expire in-the-money (just have the money to sell the stock!)

- Let the option expire worthless (out-of-the-money options are zero bid on expiration)

- Roll the put to another strike or month via a vertical spread

Implied Volatility Intro

Even if you never trade options, implied volatility (IV) can be a powerful tool. IV gives insight into a stock’s potential price movement over different time frames.

To gauge this ‘implied’ future movement, check the IV column in an options chain for any expiration cycle. Stocks that move a lot tend to have higher IV, which increases extrinsic value and inflates option prices. We can see this in the below comparison of two options chains.

Options traders love IV, especially sellers. When they believe IV is too high, they sell options, hoping the price and volatility will drop, as volatility is often not fully realized. This is a very common strategy around earnings seasons.

Long Call vs Long Put

We’ve covered long puts in detail—but how do they compare to long calls? Long calls are the opposite trade, profiting from rising stock prices, while long puts gain value when prices fall (sometimes!). Both, however, are impacted by time decay.

Long Puts and The Greeks

In options trading, the Greeks are a series of risk management tools that hint at the future price of an option based on changes in different variables. Here are the 5 most important Greeks to know:

- Delta – Measures how much the option price moves relative to the underlying stock.

- Gamma – Tracks how Delta changes as the stock moves.

- Theta – Measures time decay, showing how much value the option loses daily.

- Vega – Sensitivity to implied volatility, affecting option price.

- Rho – Measures impact of interest rate changes on the option price.

And here is the relationship between long puts and these Greeks:

Selling Put Options

Like long call options, long put options are risky bets, especially when bought out-of-the-money. Time decay works against them, meaning they lose value as expiration approaches if the stock doesn’t move in the right direction.

You may wonder—if buying put options is frequently a losing proposition, what about selling put options? Most professionals do indeed sell options. But selling naked put options introduces a lot more risk.

When you buy an option, whether a call or a put, the most you can lose is the premium paid. When you sell an option ‘naked,’ your risk substantially increases.

- For calls, since the stock can theoretically go to infinity, your risk is infinite.

- For puts, since the stock can go down to zero, your risk is substantial.

This is why you must put aside a lot of margin to sell options naked. Additionally, one lousy trade may wipe out a year's profit. This is why I have always referred to selling options naked as picking up pennies in front of a steamroller.

If you’re looking to buy a stock at a discount, selling puts can be a solid strategy. If the stock stays above the strike price, you collect the premium while you wait. If it drops to or below your strike, you’ll buy it at that level—effectively getting paid to set your buy price.

.png)

Long Put Calculator

Use our interactive calculator below to visualize the payoff of any long put option!

⚠️Besides the initial debit paid, it is essential to consider the commissions and fees associated with most options transactions when calculating the net profit or loss. These fees can significantly impact the overall return on investment and should be factored into any financial analysis or strategy planning. Read The Characteristics and Risks of Standardized Options before trading options.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

FAQ

A long put is when a trader buys a put option, betting that the stock price will drop and aiming to profit from the decline. A short put is when an investor sells a put option, collecting the premium while accepting the risk of having to buy the stock if assigned.

The maximum gain on a long put is the strike price minus the premium paid, assuming the stock drops to zero.

A call option gives the holder the right to buy a stock at a set price before expiration, typically used when expecting the stock to rise. A put option gives the holder the right to sell a stock at a set price before expiration, usually used when anticipating a price decline.

Selling a put option is more likely to succeed than buying a call since time decay works in the seller’s favor. However, this strategy is more market-neutral and has significant downside risk. With a long call, the most you can lose is the premium paid.

Long put options are not inherently riskier than long calls; both have limited risk, capped at the premium paid. However, short options can pose greater risk than long options, as they expose the seller to potentially unlimited losses (for calls) or significant downside (for puts).

You should sell a put option when you are neutral to bullish on an underlying asset. Out-of-the-money short puts are best for neutral to moderately bullish markets, while at-the-money puts offer higher premium but carry more risk of assignment if the stock moves against you.

The payoff of a long put is the difference between the strike price and the underlying asset's price at expiration minus the total premium paid. If the underlying asset's price is at or above the strike price at expiration, the long put expires worthless.

Two risks of bear put spreads include max loss and early assignment. If the stock moves above the strike prices, both options expire worthless, and you lose the entire debit paid. If the short put is in the money near expiration and you already closed the long leg, you could be assigned and end up with a long stock position.