Poor Man's Covered Call: Beginner's Visual Guide

The Poor Man’s Covered Call (PMCC) is a defined-risk trade that involves buying an in the money long-dated call while simultaneously selling a shorter-term out of the money call. The short call generates income, and the in the money call acts as a stock replacement, offering similar exposure to a covered call but with less capital required.

The Poor Man’s Covered Call is a low-cost alternative to the traditional covered call. However, the two strategies differ in key ways and are not truly interchangeable. In this article, we'll show you how they both work.

Highlights

- Capital Efficiency: The Poor Man’s Covered Call replaces 100 shares of stock with a deep in the money long call, offering similiar exposure with far less capital required.

- Income Generation: The short call generates recurring premium income, offsetting time decay on the long leg and reducing overall cost basis.

- Defined Risk: The most you can lose is the debit paid to enter the trade, since you don’t actually own shares.

- Volatility Sensitivity: Rising implied volatility tends to benefit the long LEAPS call more than it hurts the short, while falling volatility does the opposite.

- Assignment Risk: High once the short call moves in the money and expiration approaches.

- Directional Exposure: The PMCC performs best in mildly bullish or neutral markets, mirroring the covered call’s payoff while capping downside to the debit paid.

What Is a Poor Man's Covered Call?

At its core, the PMCC replaces stock ownership with a long-dated in the money call, giving similar directional exposure while freeing up capital for other trades. This makes it especially appealing to traders seeking capital efficiency and steady income potential without tying up large amounts of cash.

Poor Man's Covered Call Trade Components

The PMCC has two legs:

- Long In-the-Money Call (LEAPS): Acts as a stock replacement.

- Short Out-of-the-Money Call: Generates income and is rolled regularly to keep the trade open.

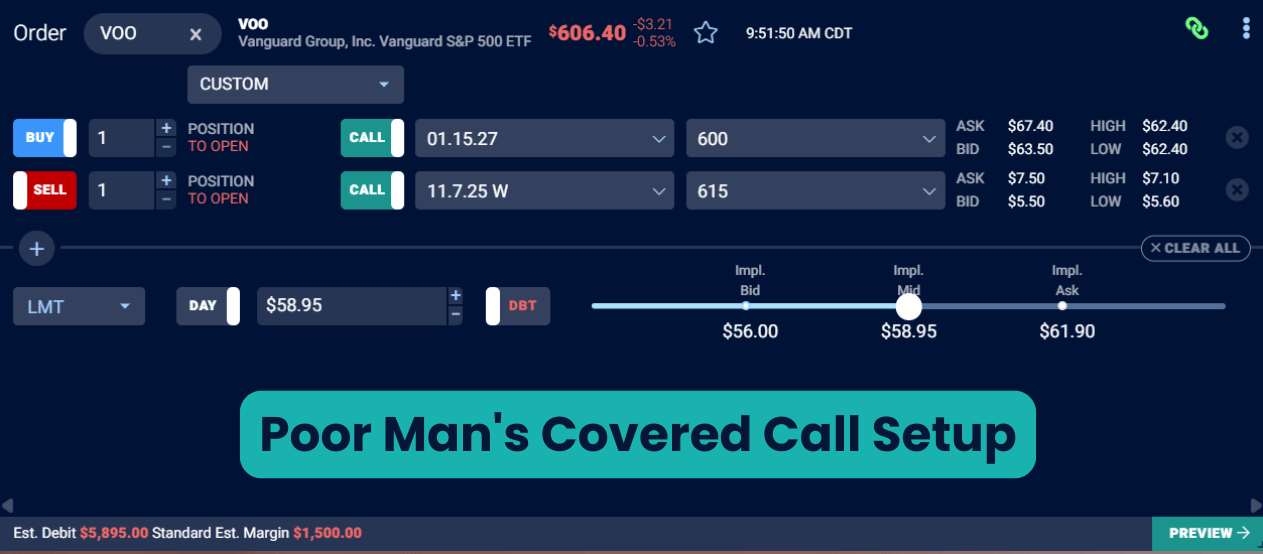

Ideally, the trade is entered in one trade (diagonal spread), as seen below on the TradingBlock dashboard:

When the short call nears expiration, you’ll need to sell a new one to keep the position active. Failing to do so leaves you holding only the long LEAPS call, which is a purely directional trade and no longer generates income.

Covered Call vs Poor Man's Covered Call

.png)

We already covered a few of the key differences between PMCCs and covered calls. Now let’s take a more complete look:

Payoff Profile

Let’s now look at the max profit, loss, and breakeven for the poor man’s covered call.

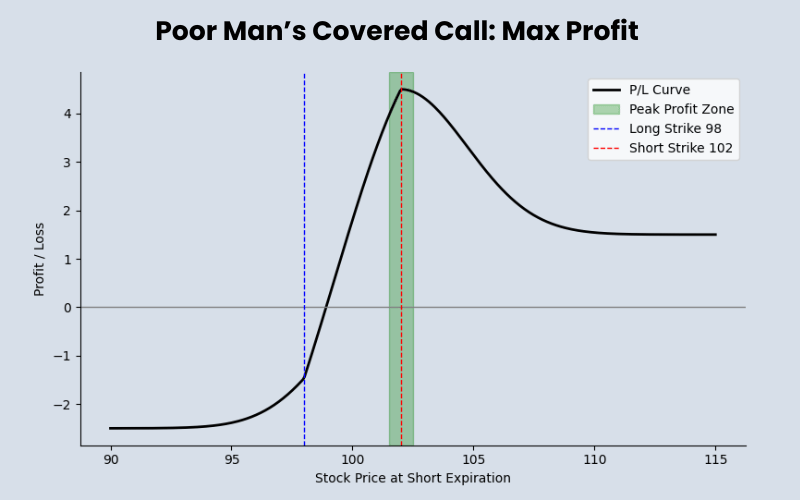

Max Profit Zone

With a PMCC, profit potential behaves similarly to a long call diagonal, which means it is undefined. The trade performs best when the stock finishes near the short call strike price at option expiration. As the short call expires, the LEAPS retains time value, allowing the position to stay open while generating recurring income.

Let’s say ABC is trading around $100, and we want to open a PMCC:

- Long Call Strike: 98 (Jan 2027 LEAPS) @ 4.50

- Short Call Strike: 102 (Mar) @ 2.00

- Net Debit Paid: 2.50

- Max Loss: $250 (the debit paid)

- Peak Profit Zone: Around the 102 short strike

The trade performs best if ABC drifts toward the short strike near its expiration. The short leg decays in value while the long LEAPS retains option premium, creating the “max profit zone.” The short call can then be rolled forward for continued income.

Max Loss Zone

The most you can lose on a PMCC is the net debit paid to enter the trade. This occurs if both options lose value and expire worthless. Even if the stock falls sharply, the loss is capped at that initial debit, since there is no stock ownership involved as there is with a covered call.

Returning to our ABC trade, the total risk is fixed at $250, which is the cost of entering the position. No matter how low the stock goes, the loss cannot exceed this amount:

- Net Debit Paid: $2.50

- Max Loss: $250

It’s worth noting that because the long call in a PMCC is typically a LEAPS, it usually retains some extrinsic value unless the stock drops significantly. This means the real-world loss is often slightly less than the full debit.

.png)

Breakeven Zone

Breakeven on a PMCC is not a fixed number because it depends on how much time value remains in the long LEAPS when the short call expires. The goal is to recover the debit paid through a mix of intrinsic value and whatever extrinsic value the LEAPS still carries.

In our ABC trade:

- Long 98 LEAPS Call @ 4.50

- Short 102 Mar Call @ 2.00

- Net Debit Paid: 2.50

If ABC finishes near $99 when the short call expires, the long 98 LEAPS is $1 in the money and still holds time value. Combined, that gets you close to covering the 2.50 debit. Of course, this depends on implied volatility, which affects how much premium the LEAPS retains. That’s why breakeven shows up as a band just under $100 in our example below.

Poor Man's Covered Call: Trade Example

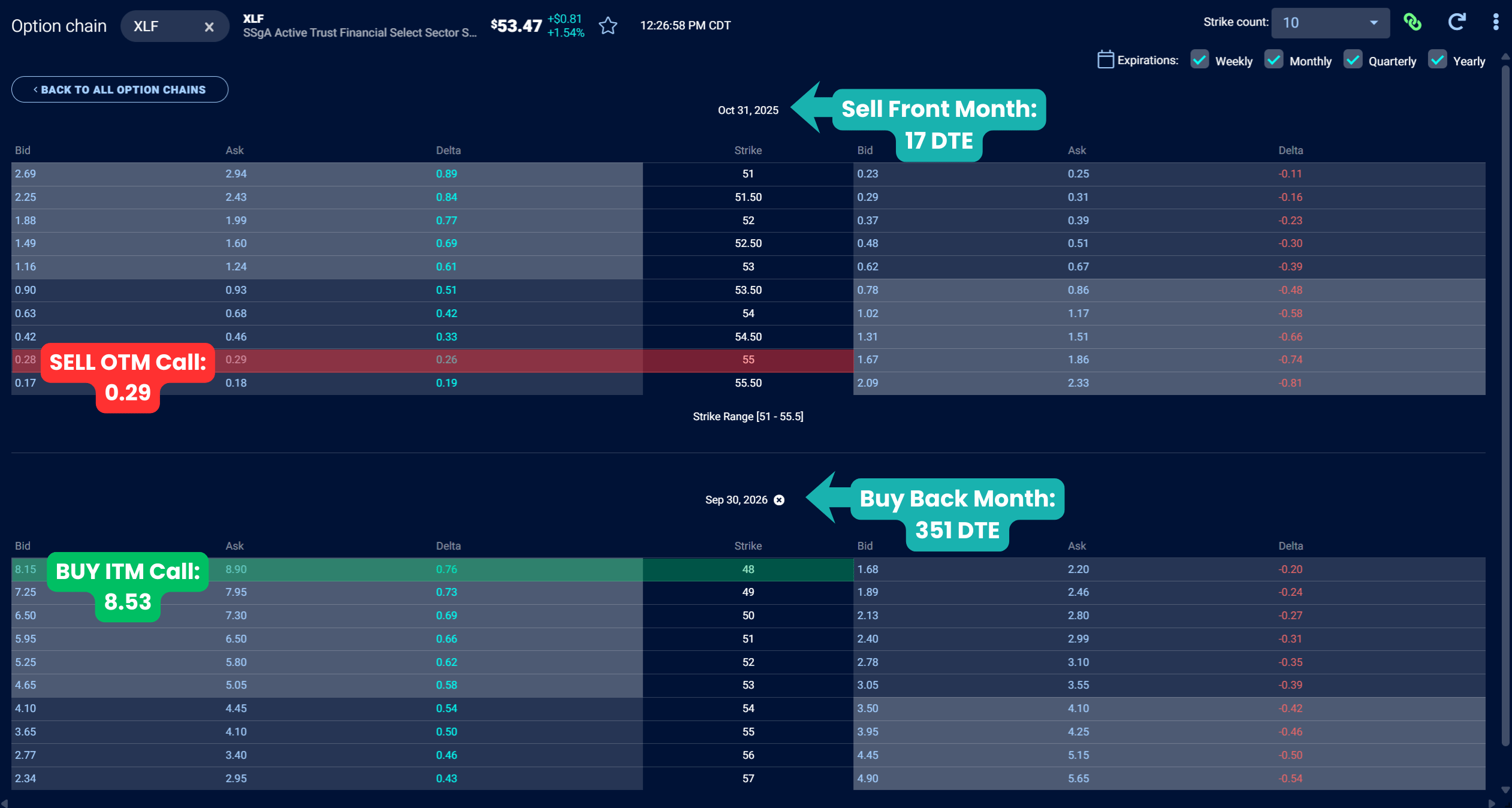

In this example, we’re going to buy a PMCC on XLF (Financial Select Sector SPDR Fund). We’re taking a long-term bullish stance on financials, but in the near term, we’ll sell a call to reduce our cost basis.

Let’s head over to the TradingBlock XLF options chain to find our expirations and strike prices.

So we’re paying $8.24 for a 7-point diagonal spread. That’s roughly 60% of the width, keeping the trade efficient and well within the recommended guideline of 75% or less of the strike width.

- The long 48 call gives us deep in the money exposure with 351 days to expiration,

- The short 55 call helps offset part of the cost with 17 days to go.

Our risk is capped at the debit paid, and our ideal outcome is for XLF to drift higher but stay below the short strike at expiration.

As always, try the midpoint first when sending option trades. If you don’t get filled, adjust the order in penny or nickel increments. Read more about options liquidity here.

.png)

XLF PMCC Trade Details

And here are the details of the trade we just put on:

- Current XLF Price: $53.47

- Buy 48 Call (Sep 30, 2026 – 351 DTE) @ $8.53

- Sell 55 Call (Oct 31, 2025 – 17 DTE) @ $0.29

- Net Debit Paid: $8.24 ($824 total)

And here’s the payoff profile:

- Breakeven Zone: Sits just under $54 at the short expiration (depends on time value in the long call)

- Max Profit: Undefined (depends on value of the long call after the short expires)

- Max Loss: Debit paid = $8.24 ($824 total)

- Profit Range: Sweet spot near the 55 short call strike at Oct 31 expiration

- Risk/Reward: Risking $824 with upside open as long as the long call retains value

Let’s now explore a few trade outcomes.

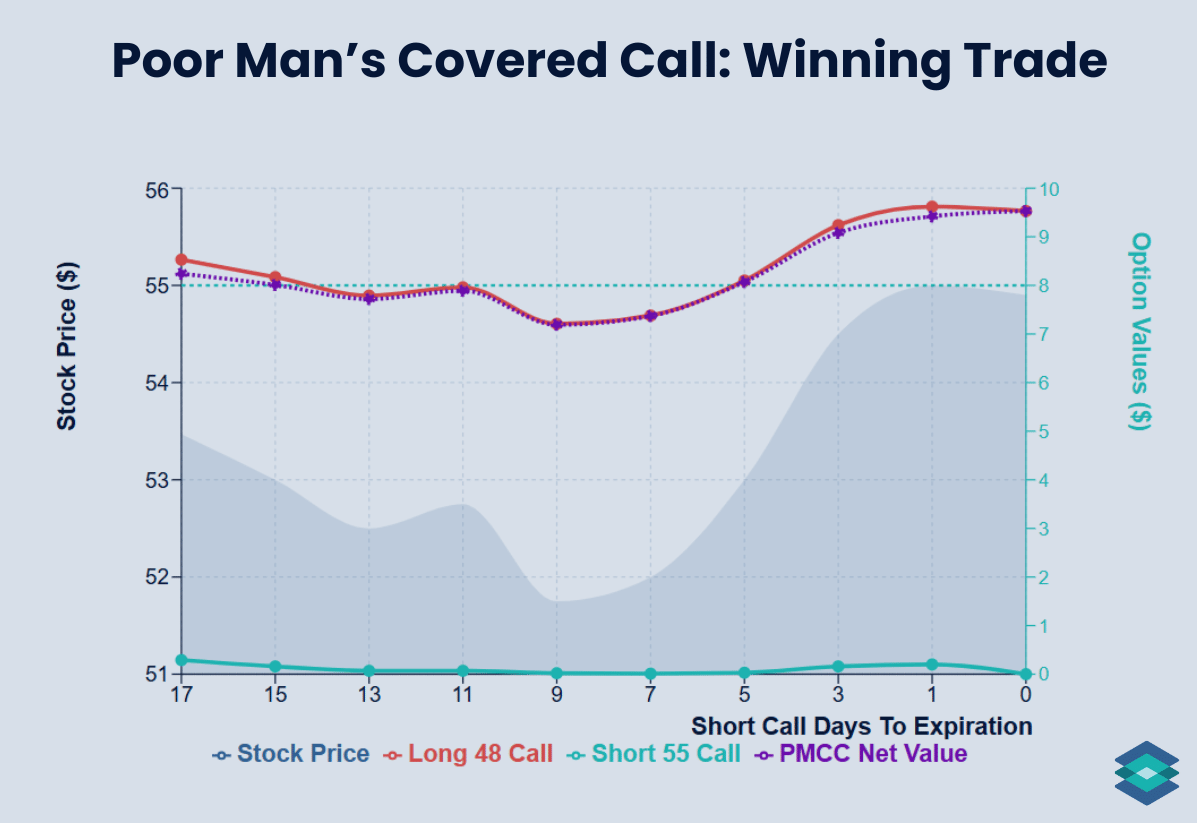

XLF PMCC: Winning Trade Outcome

Seventeen days have passed, and our short expiration is here. After a modest rally, XLF finished just below our short strike price.

- XLF Price: $53.47 → $54.90 📈

- Expiration: 17 days → 0 (short leg expires)

- Buy 48 Call (Sep 30, 2026) @ $8.53 → $9.53

- Sell 55 Call (Oct 31, 2025) @ $0.29 → $0.00 (expires worthless)

- Final Spread Value: $9.53

- Net P/L: +$1.00 ($100 total) ✅

This trade performed about as well as it could have. But remember, we still have 334 days until our long expires, which means we’ll likely sell at least a dozen more calls against it before then.

Let’s now see how this trade played out in real time.

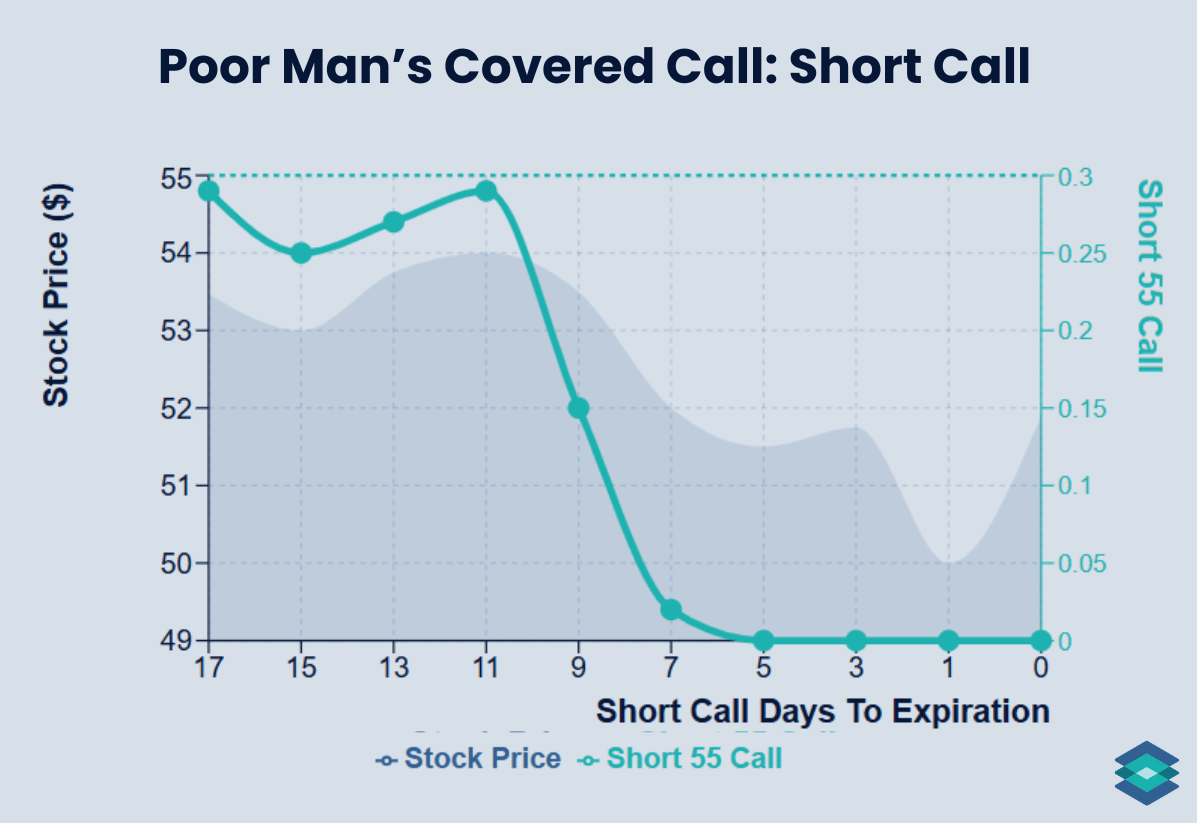

XLF Winning PMCC: Under the Hood

Here’s how our trade played out in real-time:

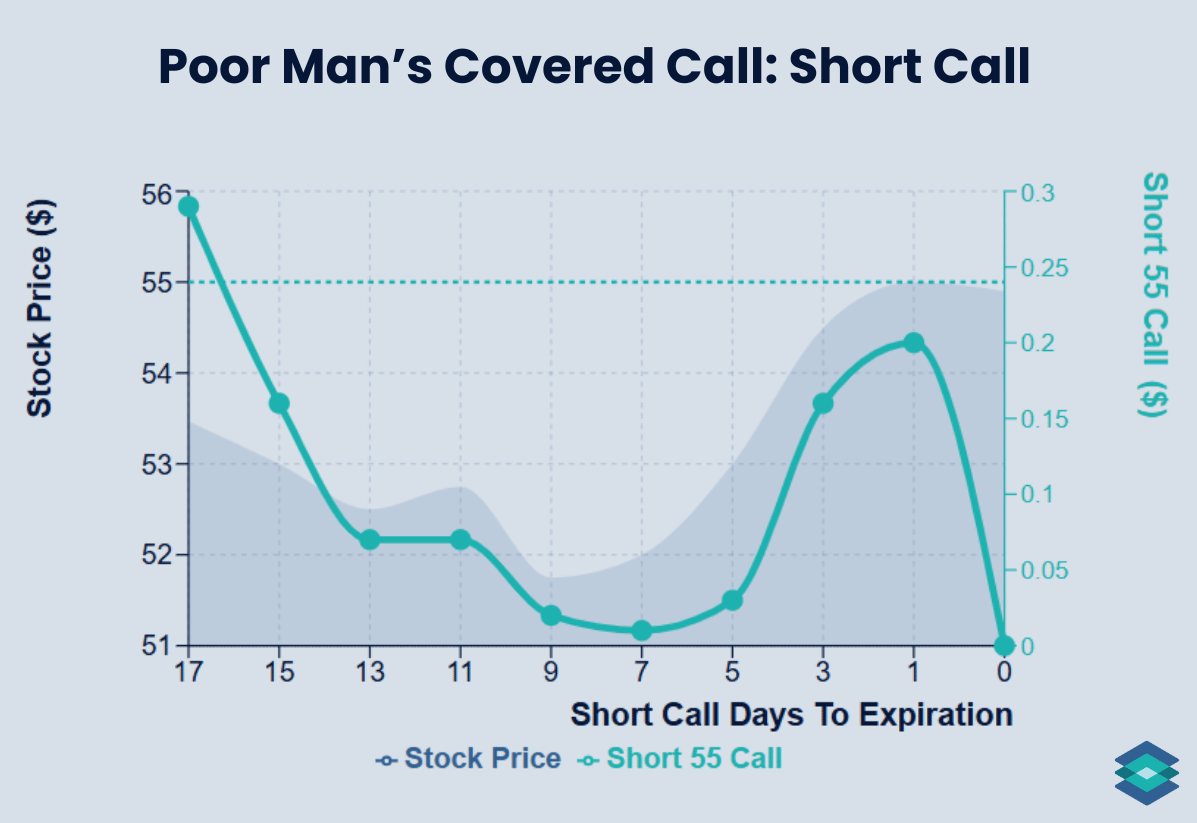

And let’s take a look at the short call represented by the teal line at the lower portion of the above graph on its own to see it on a clearer scale:

You can see how, even though the stock rallied modestly, our short call lost value as time decay accelerated into expiration. The short leg’s theta worked in our favor, while the long leg gained from its delta exposure to the underlying.

- Theta: The short call decayed quickly as expiration approached, reducing its value.

- Delta: The long call gained value as XLF moved higher.

At short option expiration, the long call increased from $8.53 to $9.53, giving us a $1.00 gain ($100 total). The short call, sold for $0.29, expired worthless, allowing us to keep that full premium.

In total, the position earned $1.29 per share, or $129 on the spread, a smooth, defined-risk profit created by a modest rally and steady time decay.

But remember, we have to sell more options before expiration to keep the PMCC alive. This trade will go through several iterations before we reach the long expiration, and there’s still plenty of risk on the horizon.

Let’s next see what happens when things don’t go our way!

XLF PMCC: Losing Trade Outcome

Seventeen days have passed, and this time the trade didn’t go our way. Instead of drifting higher, XLF pulled back slightly, pushing our long call’s value lower and eating into the premium we collected from the short leg.

- XLF Price: $53.47 → $51.90 📉

- Expiration: 17 days → 0 (short leg expires)

- Buy 48 Call (Sep 30, 2026) @ $8.53 → $7.25

- Sell 55 Call (Oct 31, 2025) @ $0.29 → $0.00 (expires worthless)

- Final Spread Value: $7.25

- Net P/L: –$0.99 (–$99 total) ❌

Even though our short call expired worthless, the decline in the long call outweighed that small gain. The pullback in XLF reduced both intrinsic and extrinsic value, while time decay chipped away at the long option

XLF Losing PMCC: Under the Hood

Here’s how our trade played out in real time.

And here’s the short 55 call to scale:

You can see how the short 55 call decayed right on schedule, while the long 48 call sold off as XLF fell from $53.47 to $51.90. Theta worked in our favor on the short leg, but delta moved against us on the long. The result was a net loss, even though the short call expired worthless.

- Theta: The short call’s premium bled out quickly as expiration neared, just as planned.

- Delta: The long call’s value fell with the underlying, offsetting the benefit of the short call’s decay.

Had we put on a straight covered call instead, here’s how the math shakes out.

- Covered Call: The stock dropped from $53.47 to $51.90, a loss of $1.57 per share. Subtract the $0.29 premium kept from the short call, and the total loss comes to –$128 on $5,347 capital (–2.4%).

- PMCC: The long 48 call fell from $8.53 to $7.25 while the short 55 call expired worthless, resulting in a –$99 loss on $824 capital (–12.0%).

The PMCC gave up less in dollar terms but showed a steeper percentage loss because it uses far less buying power than a covered call.

Poor Man's Covered Call: Strike Prices & Delta

Without understanding the option Greek delta, you’re flying blind in this trade. This is because delta tells you how much your option’s price is expected to move for every $1 change in the underlying stock. It’s the foundation for gauging directional exposure.

Among other things, delta also tells us:

- The number of shares an option ‘trades like’

- The probability that an option has of expiring in the money

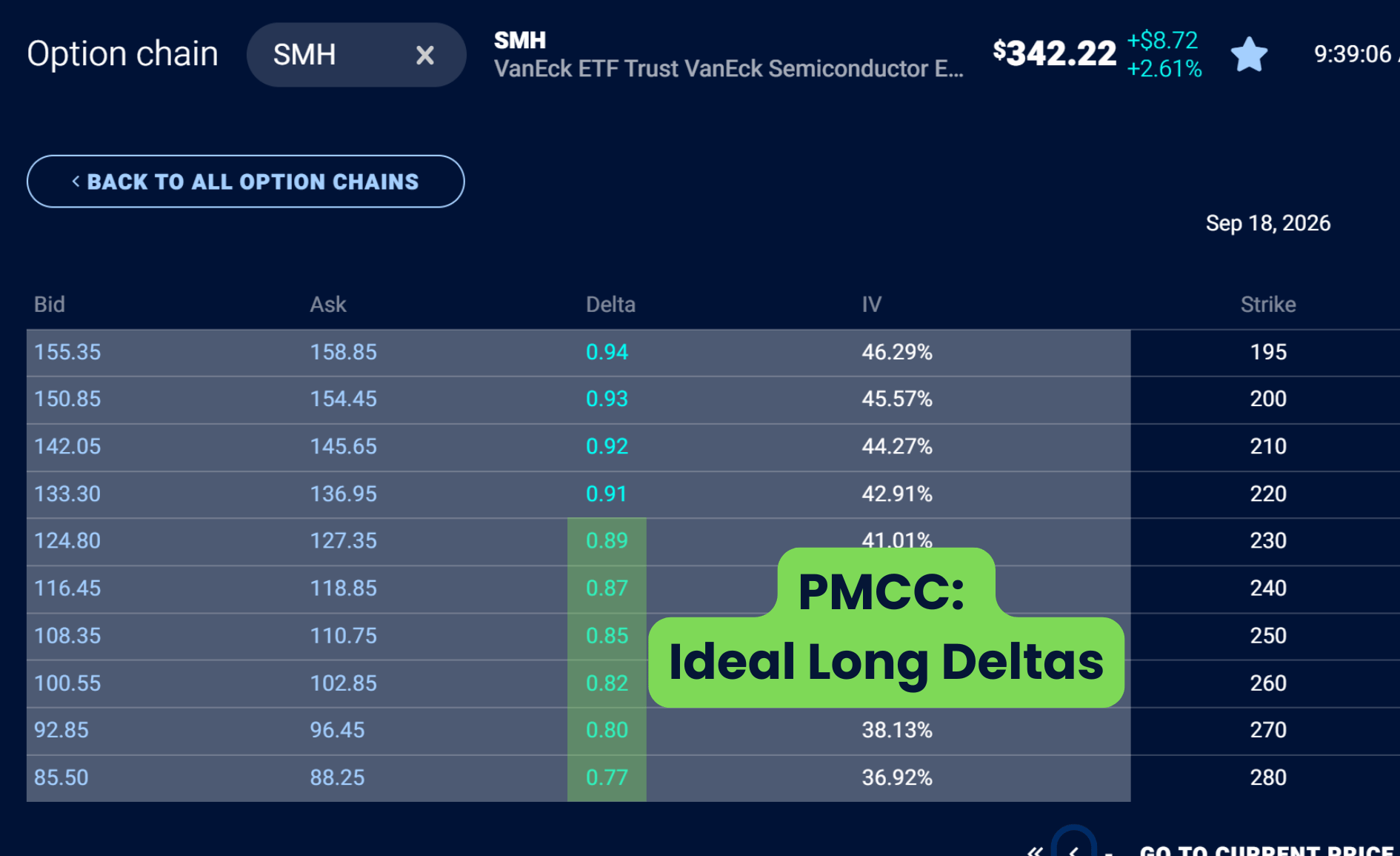

PMCC: Long Leg Delta

Since our long leg is meant to mimic 100 shares of stock, we want a high delta, preferably above 0.75 (~75 shares), so the long call closely tracks the underlying while still requiring far less capital than owning the shares outright.

You can see my ideal deltas for the long leg of a PMCC on the TradingBlock options chain below for SMH (VanEck Semiconductor ETF).

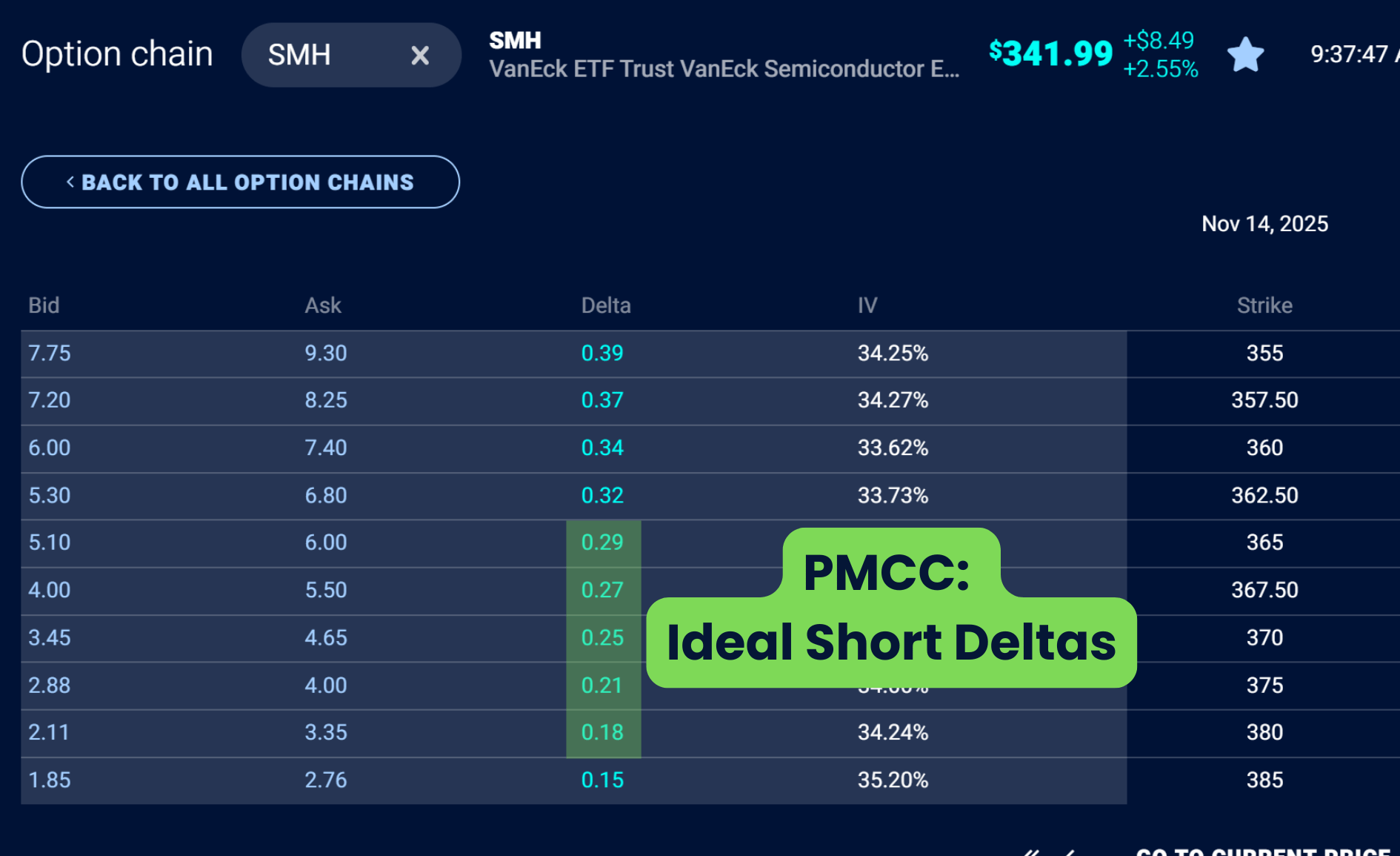

PMCC: Short Leg Delta

Delta also represents the probability that an option will finish in the money, so managing it helps balance income potential with assignment risk. Remember, we want the short leg of our PMCC to expire worthless.

- Upper limit: Stay below 0.30 delta to reduce the odds of assignment while still earning solid premium. Once you get above 0.35, assignment risk rises quickly, especially near expiration.

- Lower limit: Avoid going below 0.15 delta, since premiums become too small to justify the trade.

Time Decay (Theta) and Poor Man's Covered Call

Theta measures how much an option’s value is expected to decrease each day if price and implied volatility stay constant. It’s what makes option selling profitable since option prices naturally erode as expiration approaches.

For the short leg of a PMCC, this daily decay works in your favor. Each day that passes without a sharp move in price or volatility allows you to retain more of the premium you collected. The effect speeds up as expiration nears, which is why many traders sell short calls with 10 to 45 days to expiration to capture the steepest part of the decay curve.

.png)

Before your short expires, you’ll want to roll it out to another expiration within the above time range. Without the short component, you’re simply holding a long call with high directional exposure and no income offset, which defeats the purpose of the PMCC.

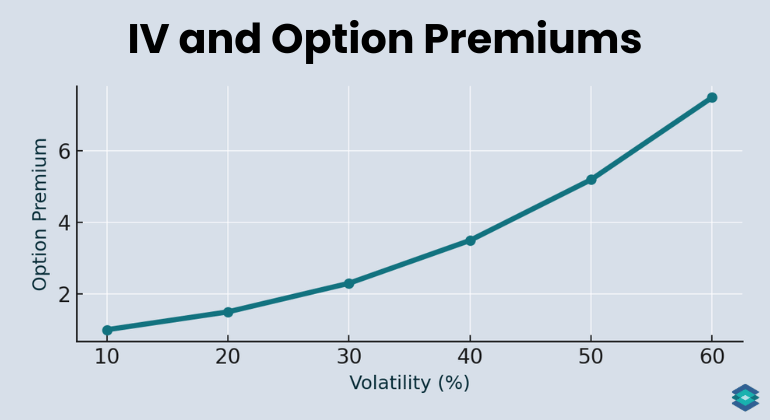

Poor Man's Covered Call and Implied Volatility

PMCCs have an interesting relationship with implied volatility (IV). IV can be thought of as a tide that lifts all ships. Rising IV increases the value of both options, benefiting the long leg but also inflating the short leg’s premium at the same time. The net effect depends on which side dominates.

If IV expands sharply after entry, the long LEAPS call usually gains more because it carries higher vega exposure. On the other hand, falling IV will hurt the long leg more than it helps the short.

The goal is to find balance, ideally entering the entire PMCC when IV is relatively low and expected to rise. That way, the long leg benefits from the increase in volatility while the short leg continues to generate consistent income through time decay.

Taxes and Index Options

One advantage of using a LEAPS option for your PMCC is that it changes how your gains are taxed. Because LEAPS are long-term options, any profit on that position may qualify for long-term capital gains treatment if held for more than a year.

On the short side, however, you’ll likely be hit with short-term capital gains (assuming your short calls expire worthless or are closed for a profit).

This is where index options can offer additional advantages. You can’t run a covered call on an index like SPX because there’s no tradable underlying security, but with a PMCC, that’s not a problem.

Index options provide two key benefits to PMCCs:

- No early assignment: Index options are European-style, meaning they can only be exercised at expiration.

- Tax efficiency: Under IRS Section 1256, index options are taxed using the 60/40 rule - 60% of gains are treated as long-term and 40% as short-term, regardless of holding period.

3 Risks of Poor Man's Covered Call

Here are a few risks to keep in mind when trading PMCCs. Keep in mind that this option strategy is not passive investing. It requires active management, and commissions can add up over time.

- Assignment Risk: If the short call finishes in the money, you could be assigned early. Managing delta and rolling before expiration helps minimize this.

- Volatility Risk: A drop in implied volatility can reduce the value of your long LEAPS call faster than the short leg decays, leading to unrealized losses even if the stock doesn’t move much.

- Directional Risk: The long call still carries delta exposure. If the underlying falls sharply, the long leg loses more value than you recover from the short premium, producing a net loss.

Poor Man's Covered Call and The Greeks

In options trading, the Greeks are a set of risk metrics that help estimate how an option’s price will respond to changes in key market variables. Here are the five most important Greeks to know:

- Delta – shows how much the option price changes for a $1 move in the stock.

- Gamma – shows how much delta shifts when the stock moves $1.

- Theta – shows how much the option loses in value each day from time decay.

- Vega – shows how much the option price changes for a 1% change in implied volatility.

- Rho – shows how much the option price changes for a 1% change in interest rates.

And here is the relationship between PMCCs and these Greeks:

⚠️ PMCCs carry unique risks that differ from standard covered calls. While the long LEAPS call limits downside to the debit paid, losses can still occur if the stock declines and the long call loses value faster than income from the short leg offsets it. Upside profit is capped by the short call, and early assignment can disrupt the trade. Results can also be impacted by changes in implied volatility, transaction costs, and slippage, which are not reflected in the examples. Always read The Characteristics and Risks of Standardized Options before trading.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

FAQ

If your short call is assigned, you’ll be required to deliver shares you don’t actually own, which effectively creates a short stock position. The easiest fix is to buy back the short stock and exit the long call in one trade, or exercise your long LEAPS call to cover the assignment.

Yes, it’s the bearish counterpart to the PMCC. Instead of a long call and short call, you use a long-dated in-the-money put and sell shorter term out-of-the-money puts to generate income.

You can simply close both legs together for a debit or credit, or roll out the short call and hold the long LEAPS if you still like the position. Many traders exit when they’ve captured 50–75% of the maximum potential profit or when the short call nears expiration.

For traders comfortable with active management, yes. It offers covered-call-like returns with far less capital.

Say XYZ trades at $100. You could buy a 90-strike LEAPS call for $12 and sell a 105-strike 30-day call for $1.50, risking $1,050 instead of $10,000 while generating similar income.

A covered call uses 100 shares of stock, while a PMCC uses a deep-in-the-money LEAPS call instead. Both involve selling an out-of-the-money call. The payoff is similar, but the PMCC requires far less capital and carries higher sensitivity to time decay and implied volatility.

A covered call is when you sell a call option against 100 shares of stock you already own. Because you hold the shares, your max profit is the premium collected plus any gains up to the strike. Your max loss is the same as owning the stock outright minus the premium collected and occurs if the stock falls to $0.

Covered calls can be considered “bad” in certain situations because the short call option limits your stock’s upside potential.